Effective Date: [April 10, 2025] Welcome to The Horizons Times By accessing or using our website https://thehorizonstimes.com , you agree to comply with and be bound by the following Terms of Use. Please read them carefully before using the Site.

1. Acceptance of Terms

By registering an account, accessing or using any part of the Site, you accept and agree to be bound by these Terms of Use and our [Privacy Policy]. If you do not agree, you should not access or use the Site.

2. Eligibility

You must be at least 16 years old to use the Site. By registering, you confirm that you meet this requirement.

3. Account Registration

You agree to provide accurate, current, and complete information during registration. You are responsible for maintaining the confidentiality of your account and password and for all activities that occur under your account.

4. Use of Content

All articles, images, videos, and other content available on the Site are protected by copyright and intellectual property laws. You may not copy, distribute, or use our content without prior written permission, except for personal, non-commercial purposes.

5. User Conduct

You agree not to:

Post or share unlawful, harmful, or offensive content.

Violate any applicable local, national, or international law.

Attempt to interfere with the Site’s operation or security.

Use bots or automated tools to collect data from the Site.

7. Termination

We reserve the right to suspend or terminate your account at any time, without notice, if you violate these Terms or if we believe your actions may harm the Site or other users.

8. Disclaimers

The Site is provided “as is” and “as available.” We do not guarantee that the Site will be uninterrupted, error-free, or secure. We disclaim all warranties, express or implied.

9. Limitation of Liability

To the fullest extent permitted by law, The Horizons Times shall not be liable for any indirect, incidental, or consequential damages arising from your use of the Site.

10. Modifications

We reserve the right to modify these Terms at any time. Changes will be effective upon posting to the Site. Continued use of the Site after changes constitutes acceptance of the updated Terms.

By clicking “I agree” or registering an account, you acknowledge that you have read, understood, and accepted these Terms of Use.

Microchips and Global Power: The New Geopolitical Battlefield

The New Cold War: The Geopolitics of Microchips

Microchips as the “New Oil” of Global Power

In the 21st-century digital economy, semiconductor microchips have become as strategically important as oil was in the 20th century. These tiny silicon wafers—packed with billions of transistors—power everything from smartphones and data centers to advanced weapons systems and critical infrastructure. In fact, microchips are often dubbed “the new oil” because of their outsized role in enabling modern technology and economic mightl. Nations are increasingly aware that leadership in semiconductors equates to geopolitical leverage in a world where computing power drives progress.

All major powers now view semiconductors as a cornerstone of national security and economic strength. Advanced chips are the foundation for cutting-edge innovations in artificial intelligence (AI), quantum computing, 5G communications, and other strategic domains. As one analyst noted, ensuring leadership in microchip technology and securing supply chains “are perhaps the preeminent economic and national security concerns of the modern era”. The global competition for semiconductor supremacy has therefore been likened to a “new Cold War,” a rivalry defined not by nuclear arms, but by silicon chips.

This report explores why semiconductors have become a central element of geopolitical rivalry and examines the roles of key players – Taiwan, the United States, China, and Europe – in the complex global semiconductor supply chain. It will analyze how microchips are used across critical sectors (from AI to defense to infrastructure) and why access to advanced chips is strategically vital. We also cover the different categories of chips (logic vs. memory, cutting-edge “advanced node” vs. “legacy” node chips), current geopolitical frictions (U.S.–China tech war, export bans, subsidy races, Taiwan’s vulnerability, etc.), and provide up-to-date data and statistics (as of 2025) with supporting sources. Throughout, we include charts and tables to illustrate key points – such as chip production by country, market share breakdowns, military applications, and R&D investments – and offer forward-looking insights into how the chip race might evolve over the next 5–10 years.

Semiconductors at the Center of Geopolitics: Why Chips Matter

Semiconductor chips are the brains of modern electronics. They serve as the fundamental building blocks for computing and digital infrastructure, which means control over chip technology confers broad power. Several factors explain why microchips have become a focal point of geopolitical rivalry:

Ubiquity in Modern Life: From trivial appliances to sophisticated weapons, chips are everywhere. “They are embedded in the control systems of devices like microwave ovens, the cores of smartphones and cars, and weapon systems,” providing essential computing power. The global economy literally runs on chips – a fact made clear by the 2020–2021 chip shortages that hampered automobile production and other industries worldwide.

Enabler of Advanced Technologies: Breakthroughs in AI, supercomputing, telecommunications, and robotics all depend on advanced semiconductors. For example, training cutting-edge AI models requires powerful graphics processing units (GPUs) or tensor processing units (TPUs) running on the latest process nodes. 5G networks, cloud computing services, and autonomous systems likewise need high-performance chips. The nation that leads in producing and deploying these chips gains a critical edge in developing future technologies – and by extension, military and economic advantages.

Military and Security Implications: Virtually all modern defense systems rely on semiconductors for their functionality. Smart missiles, stealth fighter jets, secure communications, radar and satellite systems – all are powered by advanced microelectronics. During the Cold War, U.S. strategists recognized that superior semiconductors could offset adversaries’ advantages in conventional forces. Today’s great-power competition has a similar dynamic: cutting off a rival’s access to high-end chips can cripple their ability to develop next-gen weapons or intelligence capabilities. (Notably, Western-made chips were found inside captured Russian military equipment in Ukraine – for instance, a single Russian Kh-101 cruise missile contained at least 35 U.S.-made chips from firms like Texas Instruments, Altera/Intel, and Micron. This underscores how dependent even rival militaries are on global chip technology.)

Economic Competitiveness and Industrial Strength: Semiconductor technology is a driver of productivity and innovation across industries. Countries with strong domestic chip capabilities support high-value manufacturing and tech ecosystems (e.g. Silicon Valley in the U.S., or Taiwan’s high-tech sector). Chips are also a major trade commodity – the global semiconductor market was worth $556 billion in 2021, and despite a cyclical dip in 2023, it surged to an estimated $627 billion in 2024. Controlling a larger slice of this market brings wealth and influence. Moreover, chips are required to maintain and upgrade critical infrastructure (power grids, transportation systems, telecommunications). Without secure access to semiconductors, entire economies can grind to a halt.

In short, microchips are now seen as keys to national power – vital for economic growth, military prowess, and technological leadership. This is why global powers are racing to secure supply chains and onshore production, and why policies about chips (export controls, subsidies, research funding) have moved to the top of geopolitical agendas. As U.S. Congressman Mike Gallagher put it, "semiconductors are ground zero" in the tech competition between America and China. Next, we will map out the global semiconductor supply chain and the pivotal role of each major player.

A Complex Global Supply Chain: Key Players and Chokepoints

No country today is self-sufficient across the entire semiconductor supply chain. The process of designing and manufacturing chips is one of the most complex engineering feats humans have mastered – involving dozens of specialized steps (design, lithography, etching, doping, packaging, etc.), highly advanced machinery, and a globe-spanning network of suppliers. This value chain has become highly globalized and interdependent, with different regions specializing in different stages.

Over time, four locales have emerged as especially crucial nodes in the chip ecosystem: Taiwan, the United States, mainland China, and Europe. Each plays a distinct role:

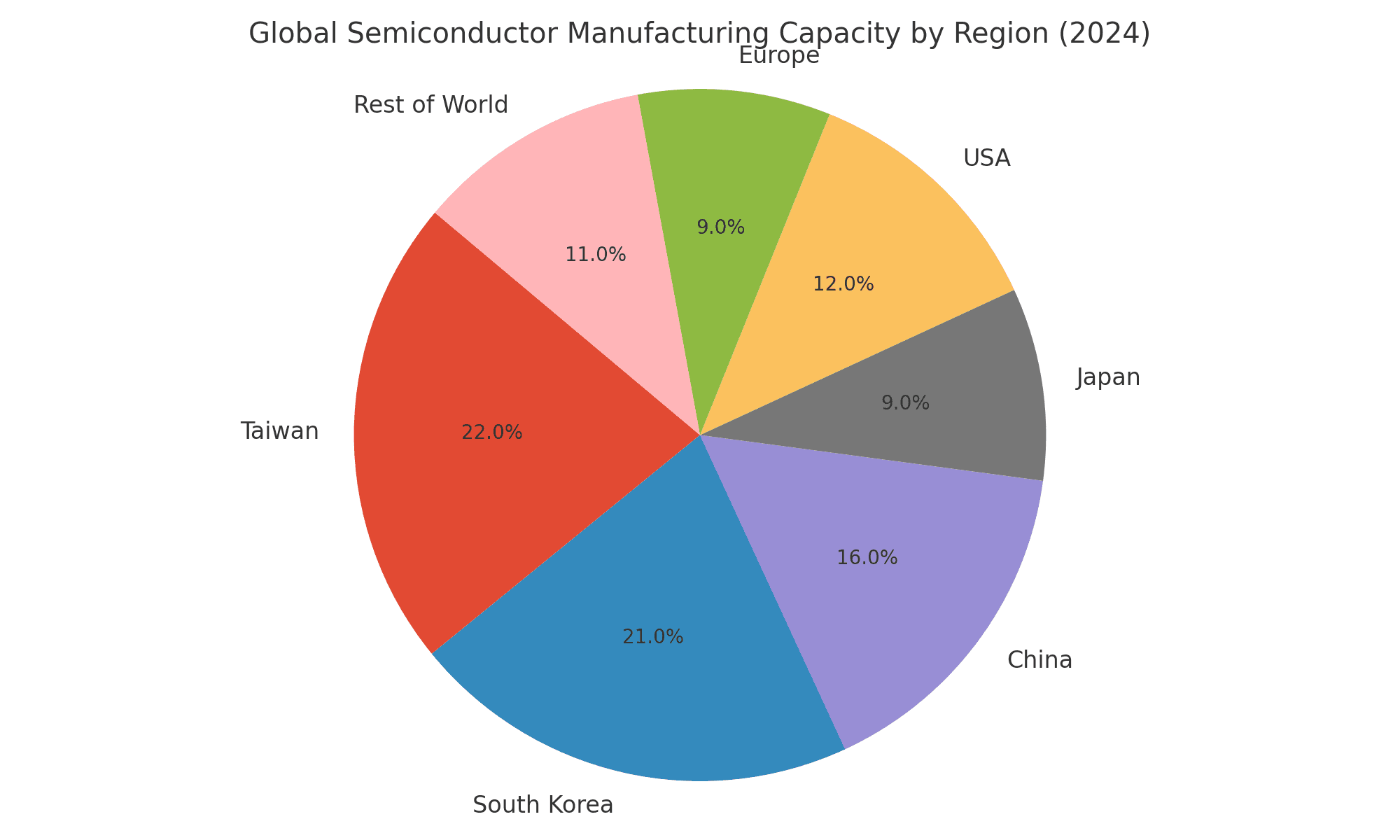

Figure 1: Global share of semiconductor manufacturing capacity by region (2021). East Asia dominates with Taiwan and South Korea alone accounting for nearly half of worldwide chip fabrication capacity. The United States and Europe, once leaders, now represent only about one-fifth combined. (Source: Knometa Research/SIA via USITC)

Taiwan: The Silicon Linchpin

Taiwan occupies a unique and outsized role in the global semiconductor landscape. This island of 23.5 million people (about half the size of Ireland) has become the world’s leading producer of the most advanced logic chips – so much so that it is often called the “Silicon Island.” Taiwan’s chip industry accounts for roughly 15% of its GDP, and its companies (led by TSMC) form an indispensable hub in the supply chain.

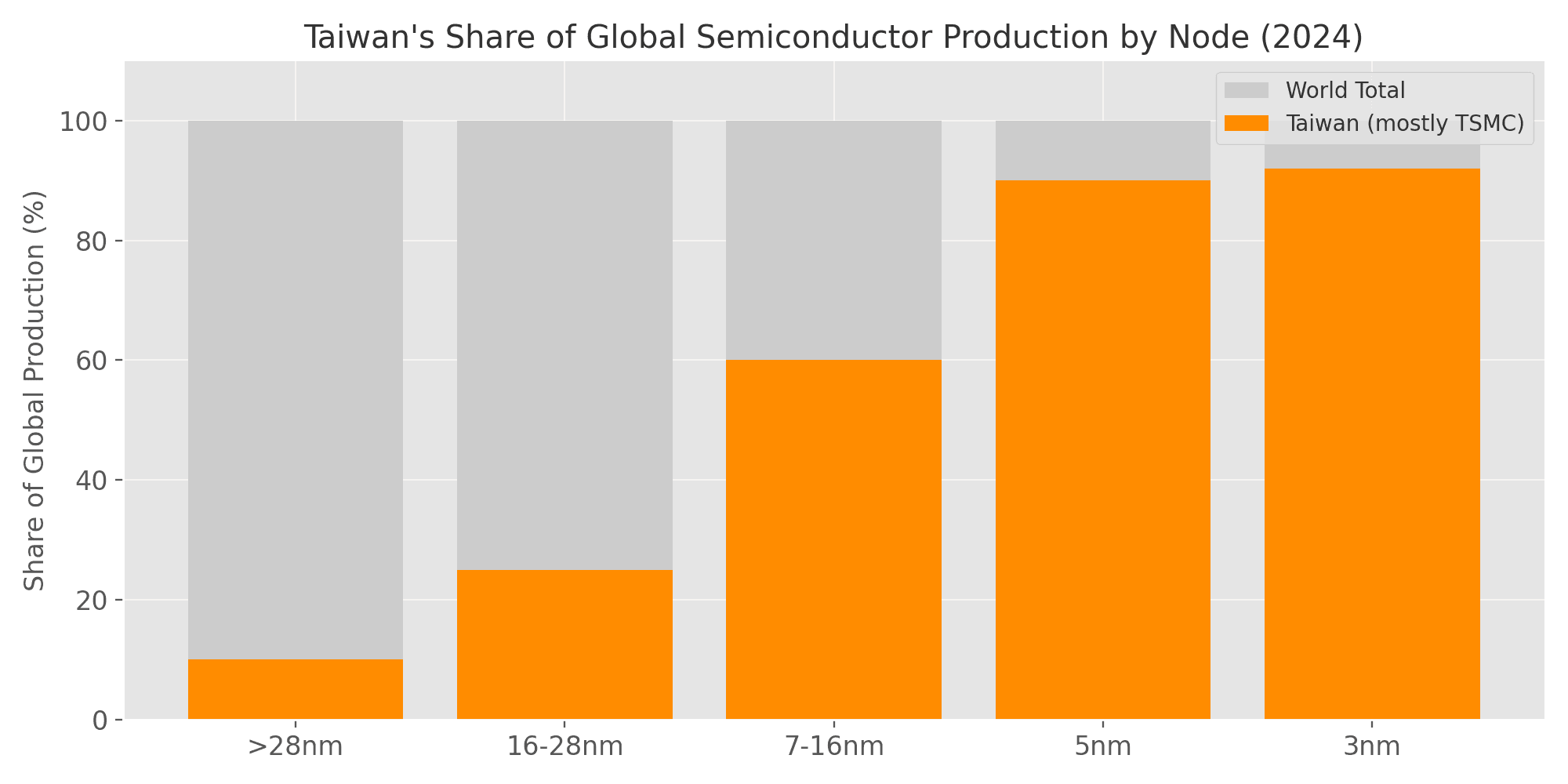

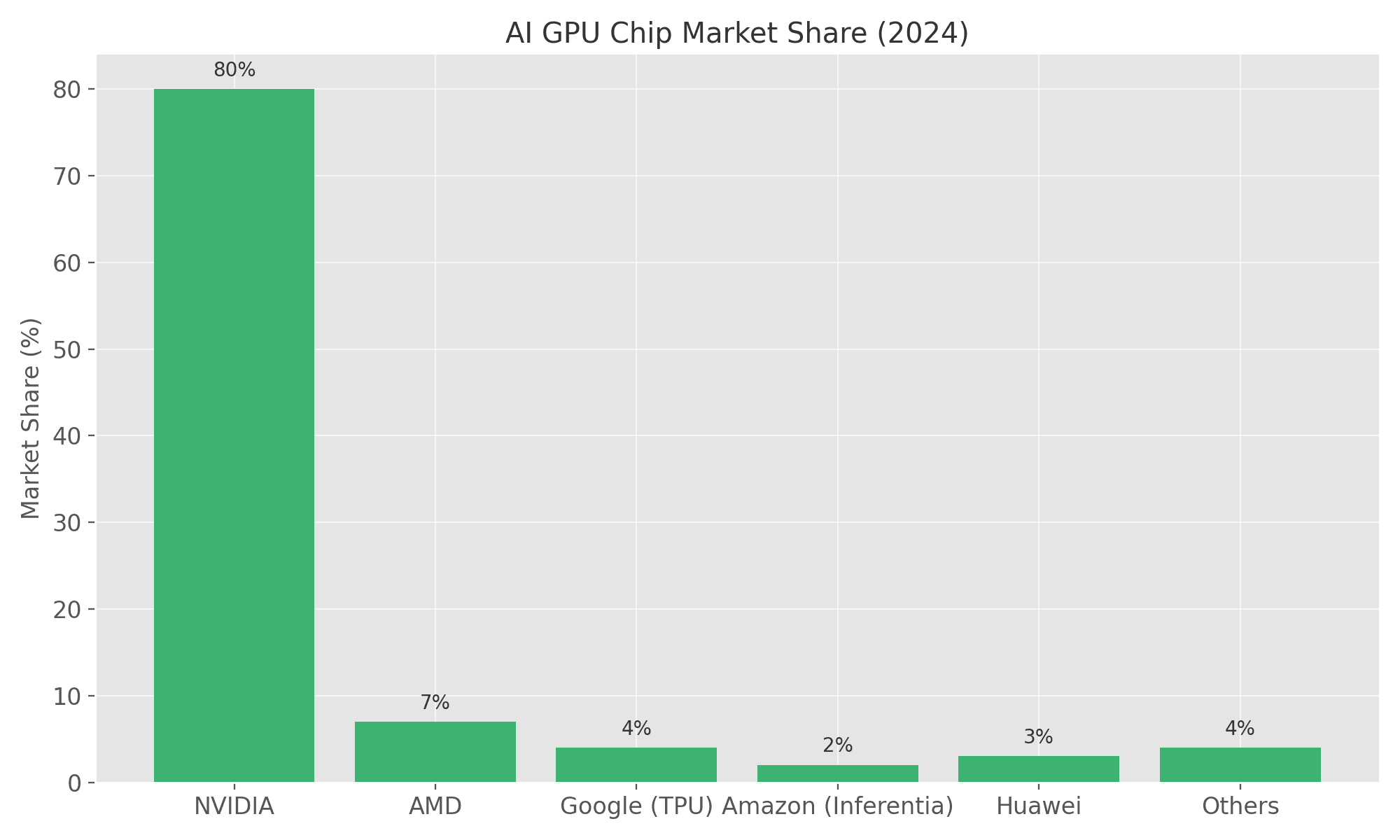

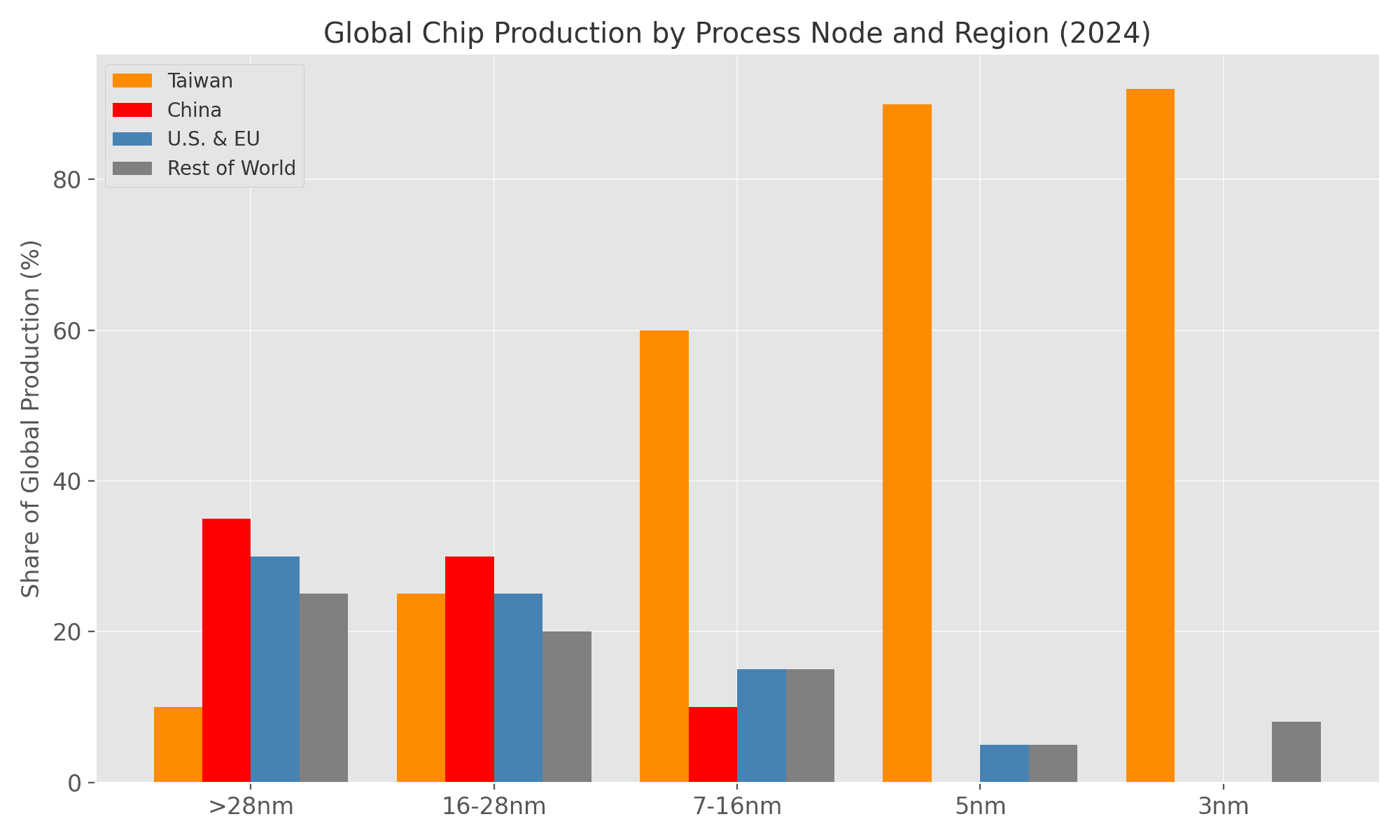

TSMC’s Foundry Dominance: Founded in 1987, Taiwan Semiconductor Manufacturing Co. (TSMC) pioneered the pure-play foundry model (fabricating chips for client companies that do not have their own fabs). TSMC is now the world’s largest contract chipmaker, manufacturing chips for Apple, NVIDIA, Qualcomm, AMD, and many others. By itself, TSMC accounts for about 50% of the global semiconductor foundry market. In cutting-edge process nodes (e.g. 5-nanometer and 3-nm chips), TSMC’s grip is even more striking – it is estimated to produce 92% of the world’s most advanced logic chips (below 10nm), essentially enjoying a near-monopoly on leading-edge manufacturing. This means that 9 out of 10 high-end processors in smartphones, high-performance computers, and advanced military systems are made in Taiwan. Such dominance has greatly profited TSMC amid the AI boom, but it also represents a single point of failure for the world.

“Silicon Shield” – Strategic Implications: Taiwan’s dominance in chips has a dual-edge effect on its geopolitical situation vis-à-vis China and the U.S. On one hand, it acts as a “silicon shield” – the idea that China would refrain from aggressive action against Taiwan to avoid disrupting TSMC’s output, which Chinese (and global) tech industries rely on heavilyc. On the other hand, it makes Taiwan an even more tantalizing target; if China were to control Taiwan’s chip fabs, it would hold a chokehold over global tech supply. This vulnerability has put Taiwan in the spotlight of U.S.–China tensions. Both Washington and Beijing are acutely aware that any conflict in the Taiwan Strait could cripple the worldwide electronics industry. As a result, Taiwan’s semiconductor prowess is seen as both a shield and a risk – prompting efforts by others to diversify away from over-reliance on TSMC’s foundries.

Local Ecosystem and Talent: Taiwan’s success is not just TSMC. The country hosts a dense ecosystem of suppliers and chip firms – from design houses (like MediaTek) to assembly and testing companies – creating what is arguably the most complete semiconductor supply chain cluster anywhere. Decades of government support, education focus, and ties with Silicon Valley (TSMC’s founder, Morris Chang, was educated and trained in the U.S.) helped seed this ecosystem. This concentration makes it efficient for companies to collaborate and produce at scale in Taiwan, further reinforcing its competitive edge.

In summary, Taiwan is the linchpin of advanced chip manufacturing globally – a position that grants it economic strength but also makes it a potential geopolitical flashpoint. Safeguarding the “Silicon Island” (or alternatively, reducing dependence on it) has become a top priority for powers like the U.S., China, and even Europe (which imports heavily from TSMC).

United States: Chip Design Leader, Rebuilding Manufacturing

The United States gave birth to the semiconductor revolution – from the invention of the transistor at Bell Labs in 1947 to the first integrated circuits in 1958. Silicon Valley remains the center of chip design and innovation, and U.S.-headquartered firms still capture the largest share of global chip revenue. However, over the past few decades the U.S. has seen a steep decline in domestic chip manufacturing, outsourcing much of the production to Asia. This decline is now viewed as a strategic vulnerability that Washington is urgently trying to reverse.

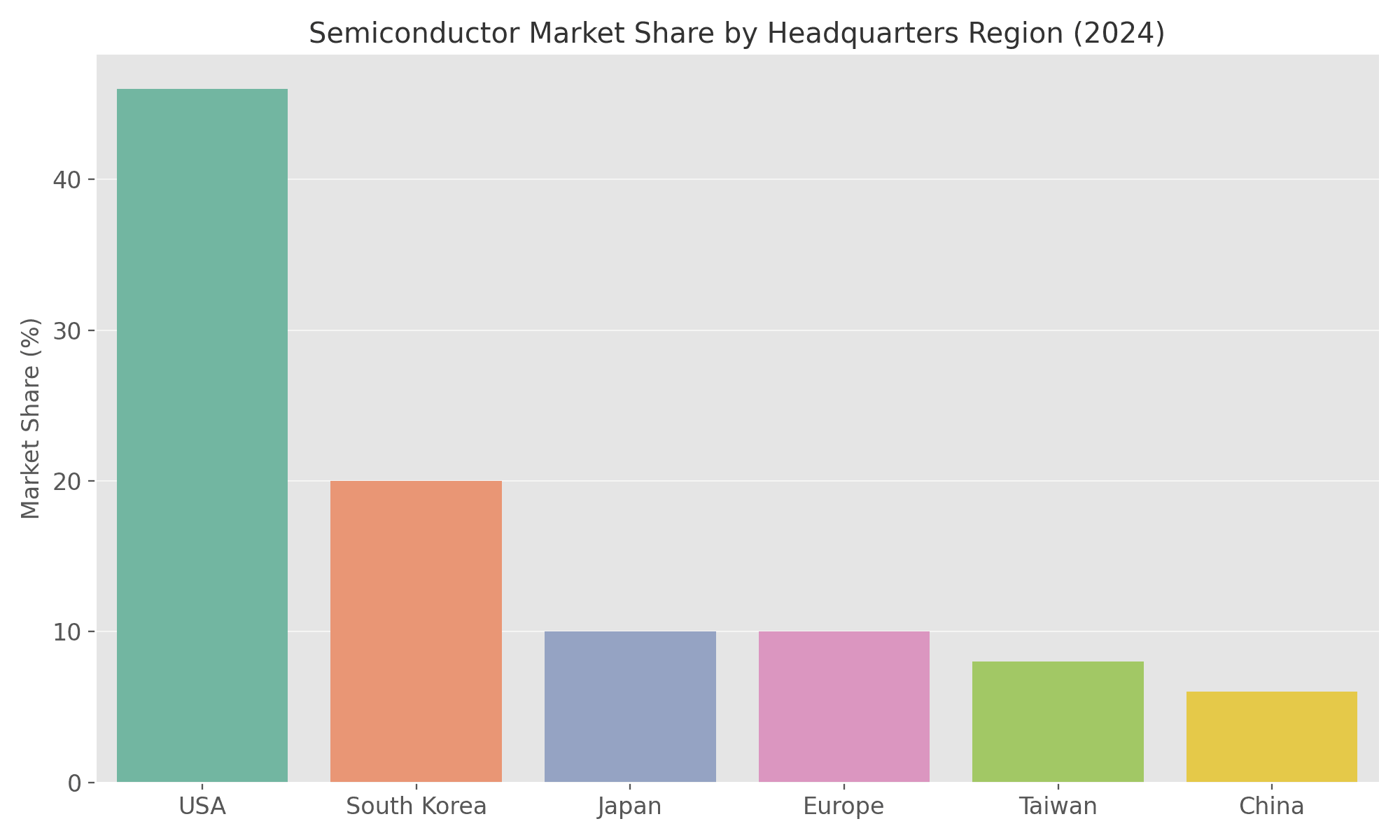

Dominance in Chip Design and IP: U.S. companies (like Intel, Qualcomm, NVIDIA, AMD, Broadcom, Apple, Texas Instruments, and many more) together account for around 45–50% of global semiconductor sales – by far the largest of any single country. This reflects American strength in chip design, electronic design automation (EDA) software, and advanced R&D. For example, virtually all of the highest-performance CPU/GPU architectures (x86, ARM-based designs, GPUs, AI accelerators) have significant U.S. lineage. Even when manufacturing is offshore, the profits and intellectual property often accrue to U.S. firms. (This is why, despite the U.S. housing only ~12% of global fab capacity, U.S.-based firms command ~46% of the world market share in semiconductors.) The U.S. also leads in critical chipmaking equipment (companies like Applied Materials, Lam Research, KLA) and EDA tools (Cadence, Synopsys) – key choke-points in the supply chain.

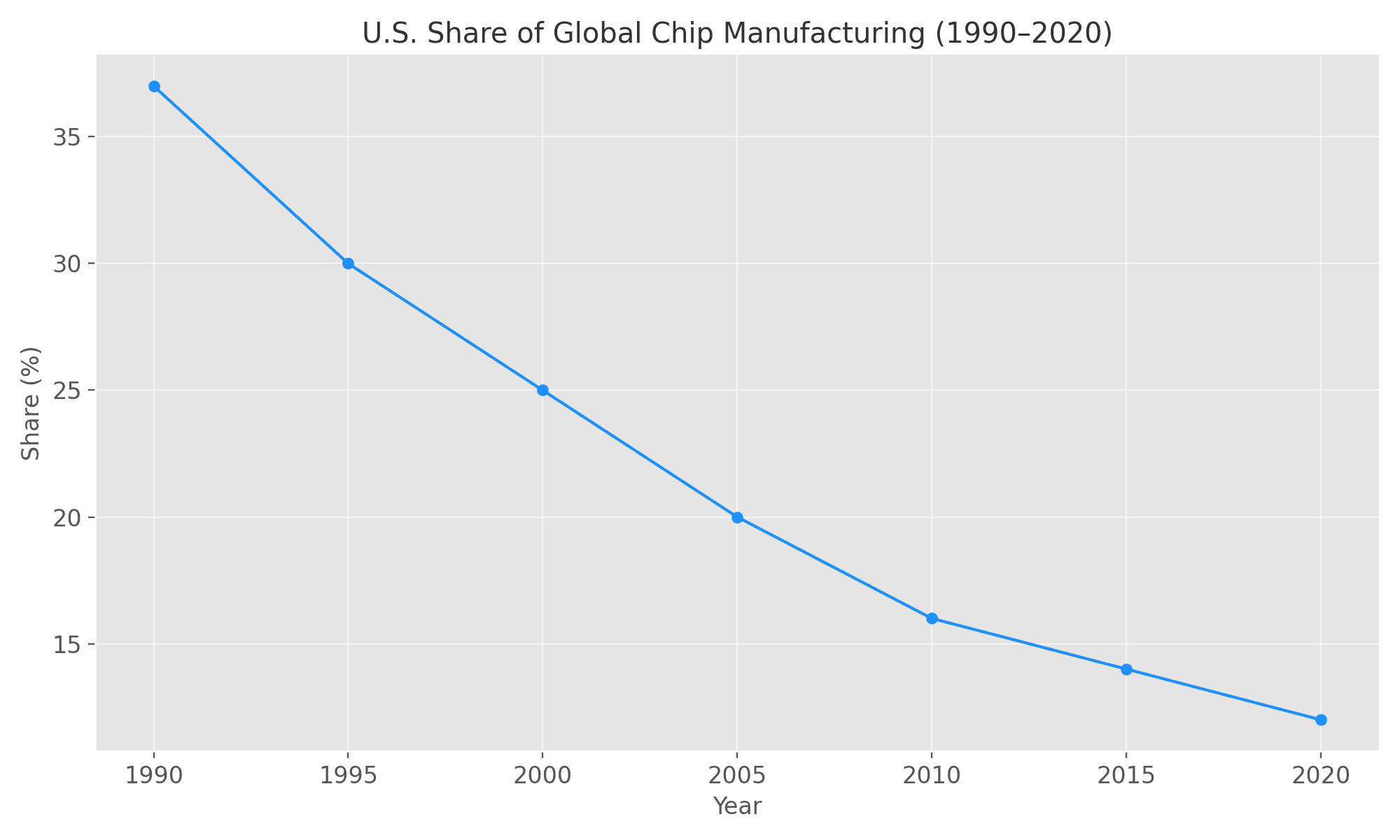

Decline of Manufacturing Share: In 1990, the U.S. manufactured 37% of the world’s semiconductors; by 2020, that fell to roughly 12%. This drop was due to high costs of operating fabs in the U.S., offshoring to lower-cost Asia, and the rise of Taiwan and South Korea. Today, America’s remaining fabs are mostly older-generation, aside from Intel’s facilities and a few specialty fabs. The overwhelming majority of cutting-edge chips used by U.S. companies are made abroad – often in Taiwan. For instance, Apple’s A-series and M-series chips, NVIDIA’s AI GPUs, AMD’s processors – all are fabbed by TSMC. Even the U.S. Department of Defense relies on Taiwanese fabs for many of its military-chip needs. This heavy dependence on foreign foundries is seen as an economic and security risk, especially after supply chain shocks and trade tensions exposed how easily things could go awry.

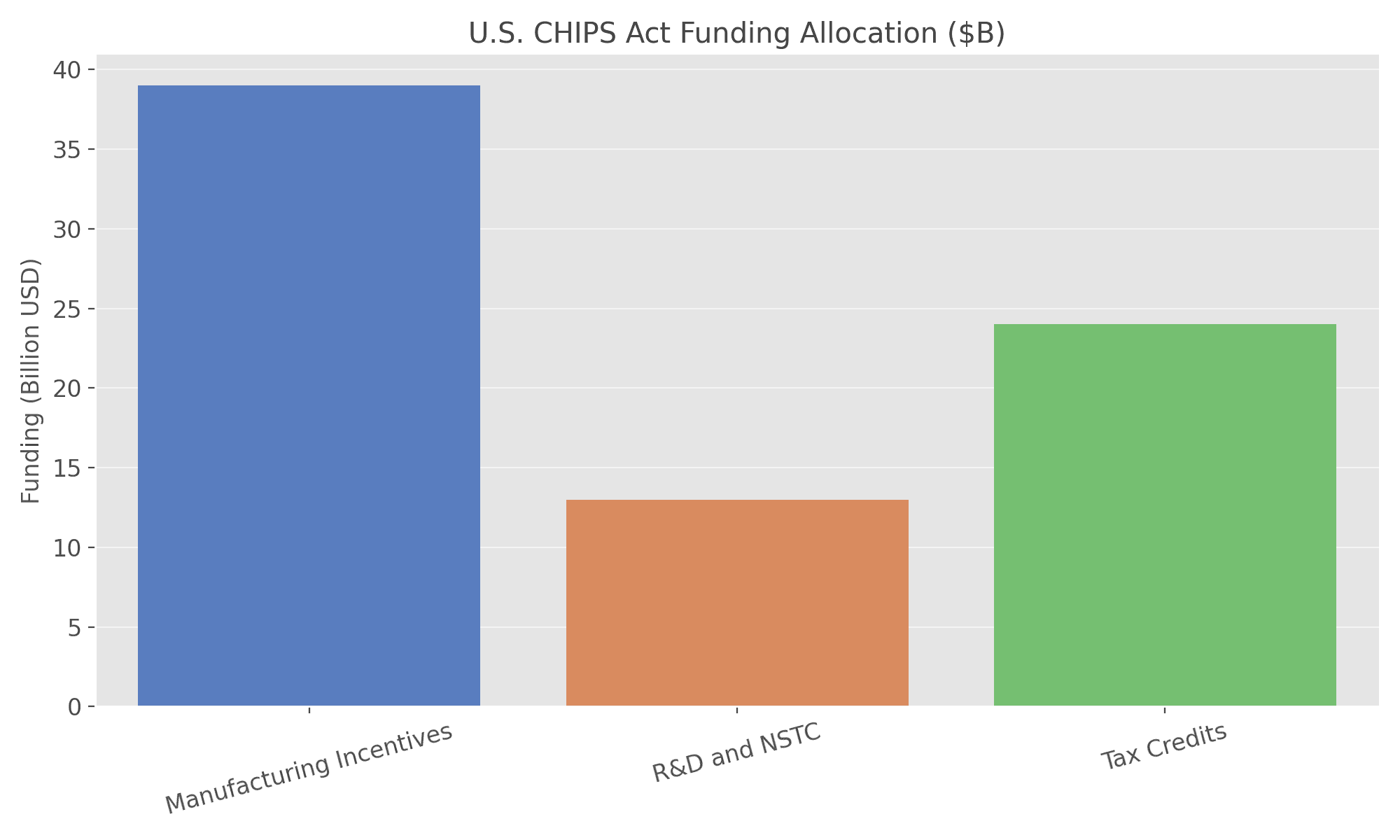

CHIPS Act and Reshoring Efforts: In response, the U.S. has launched major initiatives to rebuild domestic chip manufacturing. The centerpiece is the CHIPS and Science Act of 2022, which sets aside $52.7 billion in federal funding to incentivize new U.S. fabs and support semiconductor R&D.

Additionally, it provides tax credits for chip plant investments. This has already spurred announcements: Intel is investing tens of billions in new fabs in Arizona and Ohio; TSMC is building a fab in Arizona; Samsung is expanding in Texas (Samsung, although Korean, is a big investor in the U.S.); and Micron, TI, and others have new fab plans. The goal is to boost America’s share of global production and ensure at least the most critical chips for defense and industry can be made onshore. It’s a long-term play – new fabs take years to build – but marks a strategic shift from decades of offshoring to a mindset of "techno-industrial policy" to secure supply chains.

Strengthening Alliances and Export Controls: The U.S. is also leveraging its influence in the chip ecosystem to constrain rival powers (namely China). Because U.S. firms dominate key areas (chip design IP, EDA software, equipment), Washington has been able to impose export controls that restrict China’s access to high-end chips and tools (more on this in a later section). The U.S. has also coordinated with allies like the Netherlands (home of ASML, which makes the only extreme ultraviolet lithography machines) and Japan (another equipment/materials leader) to form a kind of “chip alliance” to maintain a collective edge over China. Meanwhile, via forums like the Quad and bilateral agreements, the U.S. is working with South Korea, Japan, and Taiwan – countries whose semiconductor industries complement America’s – to create secure supply chains among friendly nations.

In summary, the United States brings innovative prowess and economic heft in semiconductors (leading in design and R&D), and it is now investing heavily to restore manufacturing leadership at home. The CHIPS Act and similar measures aim to ensure the U.S. can produce cutting-edge chips domestically and reduce exposure to geopolitical supply disruptions. American policy is thus two-pronged: build up its own capacity while denying adversaries the same.

China: Aspiring Tech Superpower and Quest for Self-Reliance

China is the world’s largest consumer of semiconductors, yet it remains heavily dependent on foreign technology for high-end chips. In 2022, China imported an estimated $430 billion worth of chips – more than it spent on oil – underscoring its reliance. For years, China has viewed this dependence as a strategic Achilles’ heel. Beijing has therefore made achieving semiconductor self-reliance a national priority, investing huge sums in its domestic industry. However, China’s ambitions face major hurdles due to export bans by the U.S. and allies that aim to lock China out of the cutting-edge of microelectronics.

Manufacturing Growth and Gaps: China has rapidly expanded its share of global chip manufacturing in the past two decades, especially for less advanced chips. As of 2021, fabs in mainland China held about 16% of worldwide wafer fabrication capacity, up from just 9% a decade prior. This is expected to reach ~19% by 2024 as new Chinese fabs come online. However, a large portion of this capacity is for mature-node chips (28nm and above), and roughly half of China’s fab capacity is owned or run by foreign firms (TSMC, Samsung, SK Hynix, etc.) rather than Chinese companies. In leading-edge logic chips (sub-10nm), China lags far behind – its top foundry (SMIC) only recently achieved a 7nm process in limited volume (and that was reportedly by creatively using older tools). In memory, Chinese players (e.g. YMTC for NAND flash) have made some progress but still trail industry leaders in density and scale.

Largest End Market: China’s importance in chips is also as a customer. It’s the world’s largest end-market for semiconductors, accounting for ~32% of global chip sales in 2022 when counting chips that go into products manufactured in China (often for export). Chinese factories assemble a huge share of the world’s electronics – from iPhones to PCs to telecom gear – which drives massive chip consumption (even if the chips themselves are designed and made by non-Chinese firms). This gives China some leverage: disruptions in chip supply to China can hurt global electronics output. But it also means China has essentially been funding foreign chipmakers by buying so much of their product.

“Made in China 2025” and Big Investments: The Chinese government’s push for semiconductor independence has been aggressive. Policies like Made in China 2025 set targets for sourcing a higher percentage of chips domestically. China has poured tens of billions of dollars into the sector via its National Integrated Circuit funds (“Big Fund”), state subsidies, and tax breaks. In late 2022, Beijing was reportedly preparing a new 1 trillion yuan (~$143 billion) support package to bolster its chip industryreuters.com. This planned investment, spread over five years, focuses on subsidizing domestic semiconductor equipment purchases (a 20% subsidy for Chinese fabs buying local tools) and R&D. The aim is to help Chinese chipmakers leapfrog and reduce reliance on U.S. or Japanese equipment. Additionally, China is investing in talent and research, and encouraging state-owned enterprises and military suppliers to use home-grown chips even if they are slightly inferior, to drive scale.

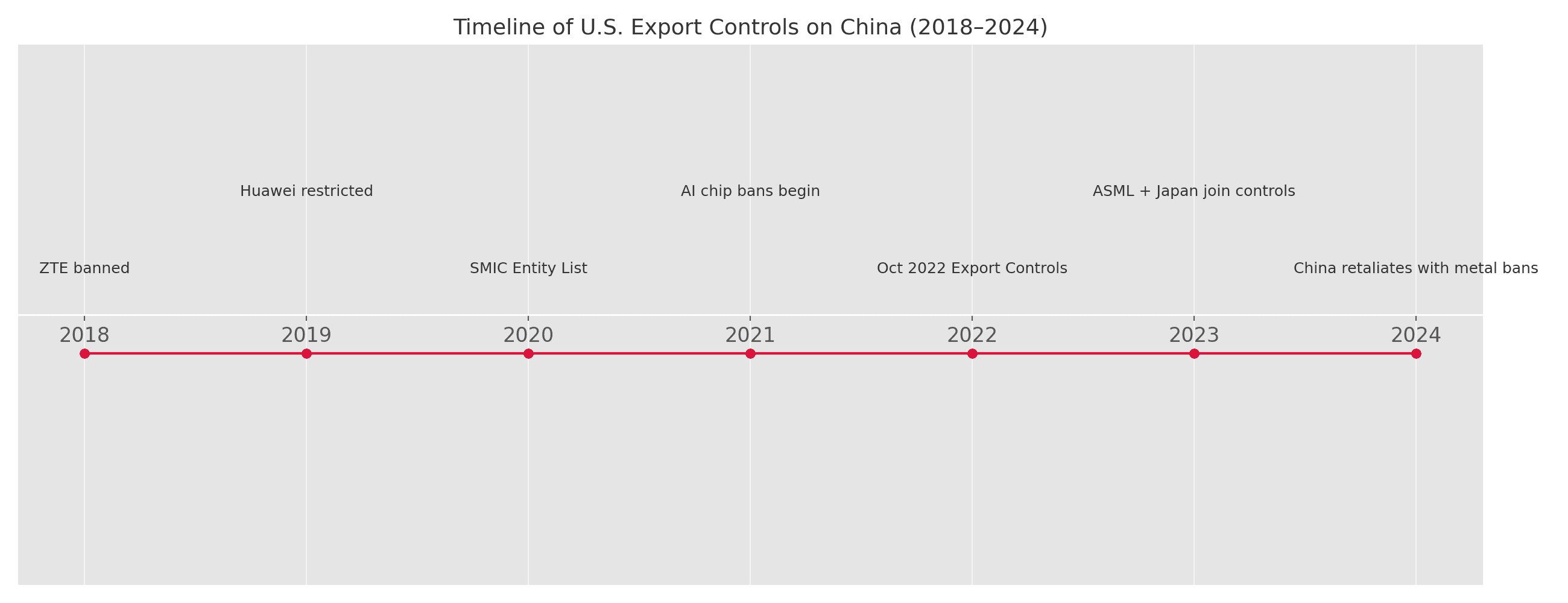

Tech War and Constraints: Despite these efforts, China has struggled at the leading edge, in part because of U.S.-led export controls. The United States has steadily tightened restrictions on China’s access to critical chip tech – from banning exports of the latest AI chips (like NVIDIA’s A100/H100 GPUs) to barring companies globally from selling China extreme lithography tools or advanced fab equipment if it contains U.S. technologyl. In October 2022, the U.S. introduced sweeping rules effectively blocking Chinese firms from obtaining chips or equipment above certain capability thresholds. The U.S. also convinced the Netherlands and Japan (home of ASML, Nikon, Tokyo Electron etc.) to align export bans on lithography and other tools in 2023. These moves have choked off China’s ability to produce cutting-edge 5nm/3nm chips, at least for now, since they can’t buy the tools or chips on the open market. In response, China has doubled down on self-sufficiency, and even retaliated by restricting exports of certain critical raw materials gallium and germanium (metals crucial for semiconductor manufacturing) in 2023 – a signal that it can also leverage its dominance in some niches (China controls 94% of global gallium supply).

Ambitions and the Road Ahead: Despite challenges, China’s long-term plan is unchanged: become a top-tier semiconductor power. By some projections, China aims to be producing 25% of the world’s semiconductors by 2030 (up from ~16% now), and to catch up in advanced node technology not long after. Enormous state-backed projects like building domestic equivalents of ASML’s lithography machines, developing indigenous chip design software, and training tens of thousands of engineers are underway. China is also focusing on areas like chip packaging, specialty chips (III-V semiconductors), and legacy nodes where it might circumvent Western choke points. In sum, China brings scale, grit, and state-driven urgency to the chip race – but breaking the current Western and Taiwanese/South Korean dominance, especially at the bleeding edge, remains a formidable challenge under export controls.

Europe: Critical Equipment Supplier and Strategic Ambitions

Europe’s role in the semiconductor domain is often underappreciated. While the European Union (EU) today accounts for only around ~8–10% of global semiconductor sales and capacity, it holds niche leadership in certain segments of the supply chain – notably in manufacturing equipment and materials, and in specific chip markets like automotive and industrial semiconductors. Recognizing the strategic importance of chips, Europe is now mounting a campaign to boost its share, with the EU Chips Act and hefty subsidies aimed at doubling production capacity by 2030.

Strength in Equipment and Materials: Europe’s most crucial contribution to the chip ecosystem is in equipment. The Netherlands’ ASML is the sole supplier of extreme ultraviolet (EUV) lithography machines, which are absolutely essential for manufacturing chips at 7nm and below. Each EUV machine costs over $150 million and there are only a few dozen in operation – without ASML’s technology, no one can make the latest chips. Likewise, companies in Germany, the UK, and France make important tools (e.g. Zeiss produces the ultra-precise lenses for ASML). European firms also lead in semiconductor materials – for example, German chemical companies and French-Italian STMicro are key suppliers. According to one analysis, Japan and Europe provide most of the raw materials and fab equipment globally – Japan accounts for ~50% of semiconductor materials and 30% of equipment production, while Europe (led by ASML) also provides a significant share. This gives Europe leverage: it can restrict sales of these to influence geopolitical outcomes (as seen when the Dutch government, under U.S. pressure, restricted ASML from selling its most advanced tools to China).

European Chip Industry: Europe once was a powerhouse in semiconductors (in the 1980s, companies like Philips, Siemens, ST were big players). Today, Europe’s chip industry is smaller but still significant in certain areas. Major European semiconductor firms include Infineon (Germany), STMicroelectronics (France/Italy), and NXP (Netherlands), which specialize in automotive, industrial, and security chips. There are also niche players like AMS, Dialog, Bosch (sensors, analog, etc.), and ARM (UK) in design (though ARM is now owned by Japan’s SoftBank). Collectively, Europe’s semiconductor industry had about a 10% global market share in 2023 (≈ $56 billion in revenue). On the manufacturing side, Europe has some capacity – for example, GlobalFoundries and STMicro operate fabs in Germany and France (mostly on 22nm, 28nm processes for auto chips), and Infineon produces power semiconductors in Europe. But Europe lacks any leading-edge logic fab – no European company manufactures at the 5nm or 3nm node as of 2025.

EU Chips Act and Investment Drive: Waking up to the strategic importance of semiconductors (and the risks of dependence on Asia), the EU unveiled the European Chips Act in 2022, with a goal to reach 20% of global chip production by 2030. The Act aims to mobilize up to €43 billion (~$47 billion) in public and private investment into Europe’s semiconductor sector, including about €5 billion dedicated to R&D for cutting-edge chip technologies. This involves building new mega-fabs in Europe through subsidies – for instance, Intel announced plans for a leading-edge fab in Germany (with ~$7 billion in German subsidies), TSMC is considering a fab in Germany as well, and STMicro/GlobalFoundries are jointly building a new fab in France with government support. The Chips Act also supports setting up pilot lines, and a network of competence centers to foster skills. Europe is essentially trying to ensure security of supply (especially for its automotive industry which was hit hard by chip shortages) and to not be left behind in the tech race. While reaching 20% share (up from ~10%) in 5 years is ambitious, these efforts underscore that Europe sees chips as strategic infrastructure.

Geopolitical Position: Europe finds itself somewhat in the middle in the U.S.–China chip war. On one hand, Europe (especially countries like the Netherlands, Germany, France) has aligned with U.S. export controls to limit China’s access to crucial tech (e.g., ASML not shipping EUV to China). On the other hand, European industries have significant markets in China (for both chips and equipment) and want to avoid a full decoupling. Europe’s strategy seems to be “open autonomy” – invest in its own capabilities and work with like-minded partners to reduce dependence on Asia, while still engaging globally. European leaders also frame the Chips Act as part of technological sovereignty – ensuring that Europe can produce what it needs for its digital and green transitions without being at another’s mercy. In security terms, NATO and EU views on protecting semiconductor supply chains align with the U.S., given the reliance of Western defense systems on advanced chips.

South Korea and Japan (Context): Although not the main focus of this report, it’s worth noting that South Korea and Japan are also key pillars of the semiconductor supply chain. South Korea (home to Samsung and SK Hynix) is the world leader in memory chips and a major player in logic foundry (Samsung is #2 after TSMC). Japan, while its share of chip production has declined from its 1980s peak, remains a top supplier of materials (silicon wafers, chemicals, gases) and equipment (Tokyo Electron, Nikon, Canon) – as well as owning important chip IP (e.g. Kioxia in NAND flash, Sony in image sensors). Samsung and SK Hynix in Korea together have about 44% of global memory chip capacity (Samsung alone is often the #1 or #2 semiconductor firm by revenue, trading places with Intel in recent years). These U.S.-allied countries are thus crucial partners in any strategy to secure supply chains vis-à-vis China. Both Korea and Japan have announced their own chip initiatives (Samsung unveiled a colossal $230 billion investment plan over the next two decades for new Korean fabs, and Japan set up a consortium “Rapidus” to develop 2nm logic chips domestically by late 2020s). The U.S., Taiwan, South Korea, Japan, and Europe collectively form a tightly interwoven network that currently produces the world’s most advanced semiconductors – a network now being fortified to maintain an edge over China.

Chips Across Sectors: AI, Defense, Economy, and Infrastructure

Semiconductors are not a monolithic product – there are myriad types of chips serving different functions, and they underpin virtually every sector of modern society. Here we analyze how microchips are used across key domains – artificial intelligence, military/defense, economic/industrial, and critical infrastructure – and why access to the most advanced chips in each area is considered strategically critical.

Artificial Intelligence and Computing

The recent breakthroughs in AI – from machine learning to large language models – have been enabled by exponential increases in computing power, which in turn are driven by advanced chips. Training AI algorithms (like deep neural networks) involves massive parallel computations on specialized processors. GPUs (graphics processing units), originally for rendering graphics, proved extremely adept at AI tasks and have become the workhorse for ML training. Newer AI-specific chips like TPUs (Tensor Processing Units) or other AI accelerators further boost capabilities. These cutting-edge AI chips are manufactured on the most advanced process nodes to pack in maximum transistors for speed. For example, NVIDIA’s A100 and H100 datacenter GPUs (crucial for AI research) are built by TSMC at 7nm or 5nm. Each time you do a Google search or use an AI service, it likely touches a server with such high-end chips.

Access to these advanced chips determines who can push the frontier of AI. Countries that can deploy more AI computing can potentially leap ahead in fields like autonomous vehicles, intelligent healthcare, fintech, and big data analytics. AI supremacy is viewed as a proxy for overall tech supremacy in the coming decades. This is why the U.S. has moved to ban exports of top AI chips to China – to constrain China’s AI development that might feed military or surveillance applications. It’s also why nations are investing in supercomputing centers and domestic AI chip design (e.g., China’s Huawei designing AI chips, Europe’s EPI initiative for HPC processors). Simply put, AI capability = chips × algorithms × data. Chips are the hardware backbone, and the most advanced chips give an edge in training more powerful AI models.

Defense and Security

Modern defense systems are extraordinarily chip-dependent. Smart weapons, command-and-control networks, satellites, encryption devices, radar and electronic warfare systems – all rely on integrated circuits. In many cases, the performance of a missile or jet is directly tied to the sophistication of its onboard electronics. For example, an F-35 fighter jet contains dozens of microprocessors and sensor chips to manage its avionics, targeting, and stealth capabilities (many of which, as noted earlier, are actually fabricated by TSMC in Taiwan) csis.org. Advanced semiconductors also power the supercomputers used for cryptanalysis and nuclear simulations, and the AI systems for intelligence analysis. Consequently, having assured access to high-performance and trusted chips is a national security imperative. The U.S. DoD has programs like the “Trusted Foundry” to certify secure chip production for sensitive military designs, but ironically as of 2021 only about 2% of chips used in U.S. military systems were made in DoD-trusted domestic foundries – the rest were commercial-off-the-shelf chips from the global market. This is a concern if supply were cut off or if malicious implants could be introduced.

Countries are increasingly worried about being cut off from chips in a crisis. The West’s sanctions on Russia’s tech imports following the Ukraine invasion illustrate this – Russia struggled to source chips for its weapons, and evidence emerged of Russian missiles using repurposed chips from home appliances due to shortages. On the flip side, China’s military modernization (from hypersonic missiles to AI-driven drone swarms) will falter if it cannot get or produce advanced semiconductors. Electronic warfare and cyber defense also revolve around who has better chips. For instance, secure communications and code-breaking often demand super-fast processors. It’s telling that the Pentagon lobbied heavily for the U.S. CHIPS Act to ensure American fabs stay at the cutting edge. In summary, semiconductors play a role in every aspect of national defense, and cutting-edge chips can act as force-multipliers. Maintaining a lead in defense-related microelectronics (and denying the same to adversaries) is viewed as crucial for military balance.

Economic, Industrial, and Infrastructure Applications

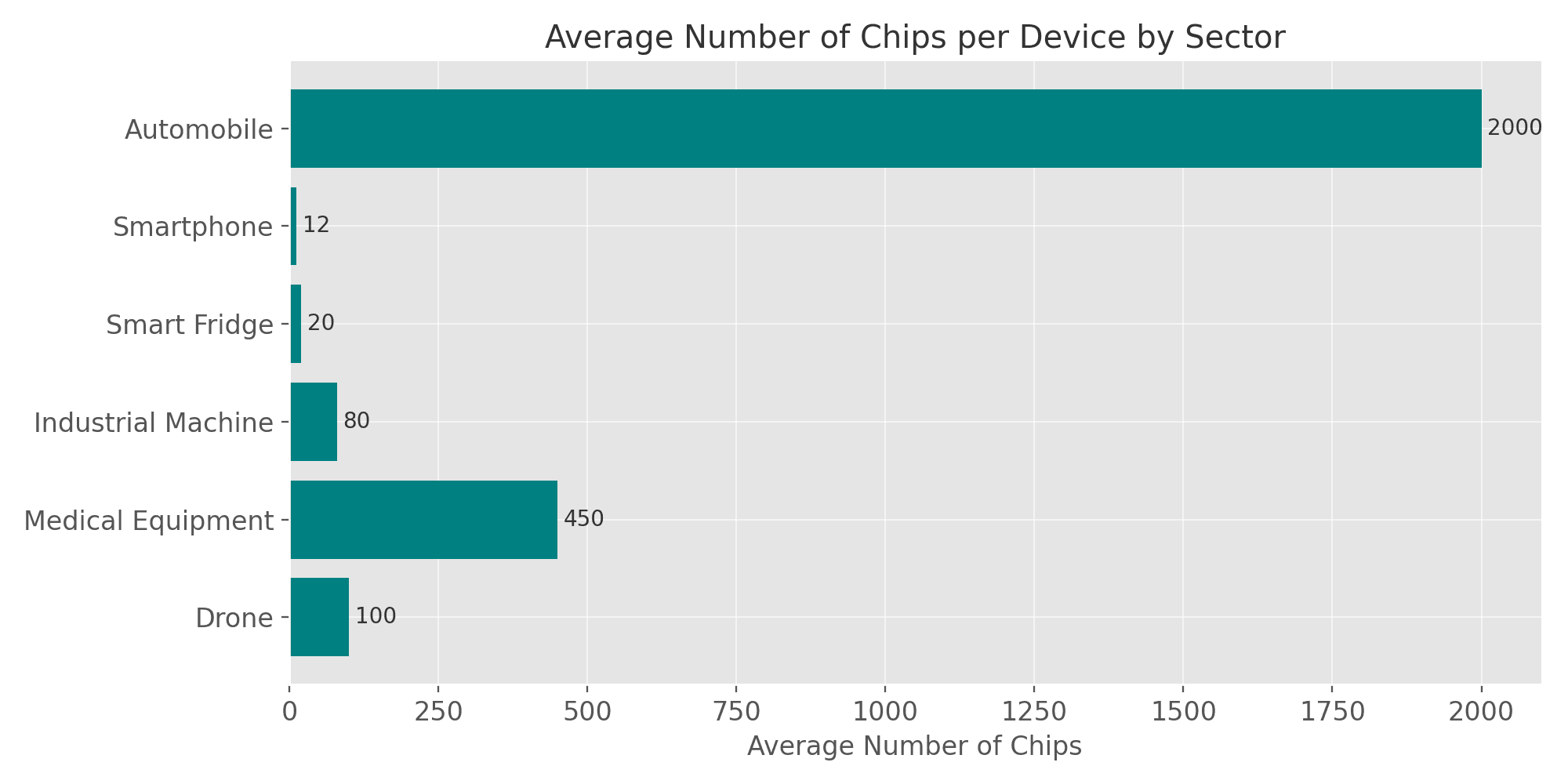

Semiconductors are the engines of the modern economy. A single smartphone can contain a dozen chips (applications processor, memory, RF transceivers, power management ICs, sensors, etc.). A modern automobile has on the order of 1,000–3,000 chips embedded, controlling everything from engine timing to ABS brakes to infotainment systems. High-end electric vehicles and autonomous cars have even more semiconductor content (for battery management, lidar, AI driving systems). In manufacturing and critical infrastructure, chips are ubiquitous: factory robots use microcontrollers and sensors; power grids use specialized chips for load management; trains and aircraft have numerous control chips; medical devices like MRI scanners or even pacemakers rely on chips. The advent of the Internet of Things (IoT) is adding billions of connected devices, each with at least one microchip “brain” inside.

Because of this pervasiveness, economic security is tied to chip security. The 2020–2021 global chip shortage demonstrated how a lack of even relatively simple “legacy” chips (like those used in car ECUs) can halt car assembly lines and cause billions in losses. It’s not just the fancy 5nm chips; even a shortfall in 28nm microcontrollers can disrupt supply chains. Nations are now keenly aware that semiconductor supply disruptions = economic disruptions. This has prompted efforts to diversify sources and stockpile critical semiconductors for key industries. For instance, Japan and Europe both initiated programs to support more local production of automotive and industrial chips after the shortage exposed heavy reliance on Taiwan for these as well.

Infrastructure and national development also hinge on chips. Consider telecommunications: 4G/5G base stations use high-end radio frequency chips and processors (where firms like Nokia, Ericsson, Huawei, ZTE compete). Energy: modern smart grids or solar inverters contain power electronics. Transportation: air traffic control and modern railway signaling depend on reliable semiconductors. Even agriculture uses GPS-guided tractors with chips. In essence, virtually every critical infrastructure sector has become digitized and “chip-ified.” Governments now include semiconductors in their definition of critical infrastructure that needs protection and resilience.

One particular area of concern is the dual-use nature of advanced chips: the same GPU that accelerates AI for healthcare can also train AI for military drone targeting; the same chip that runs a smart city’s traffic system could be used in a cyber warfare center. Thus, controlling who has access to what level of chip technology is seen as strategically vital not just for pure defense, but for economic and societal stability.

In economic terms, securing advanced chips is also about securing the industries of the future. Countries want to ensure they are not left behind in the “Fourth Industrial Revolution” – which includes AI, IoT, autonomous systems, etc. – all of which require semiconductors. That is why we see huge government incentives to build fabs and ambitious R&D programs to push the envelope (discussed later). It’s an investment to anchor high-tech economic activity domestically and reap the downstream benefits (jobs, innovation hubs, etc.).

Not All Chips Are Equal: Logic, Memory, and Legacy Nodes

When discussing microchips, it’s important to distinguish between different types of chips and different levels of technology. Geopolitical competition spans all these types, though in different ways. The major categories include logic vs. memory chips, and leading-edge (“advanced node”) vs. mature (“legacy”) processes.

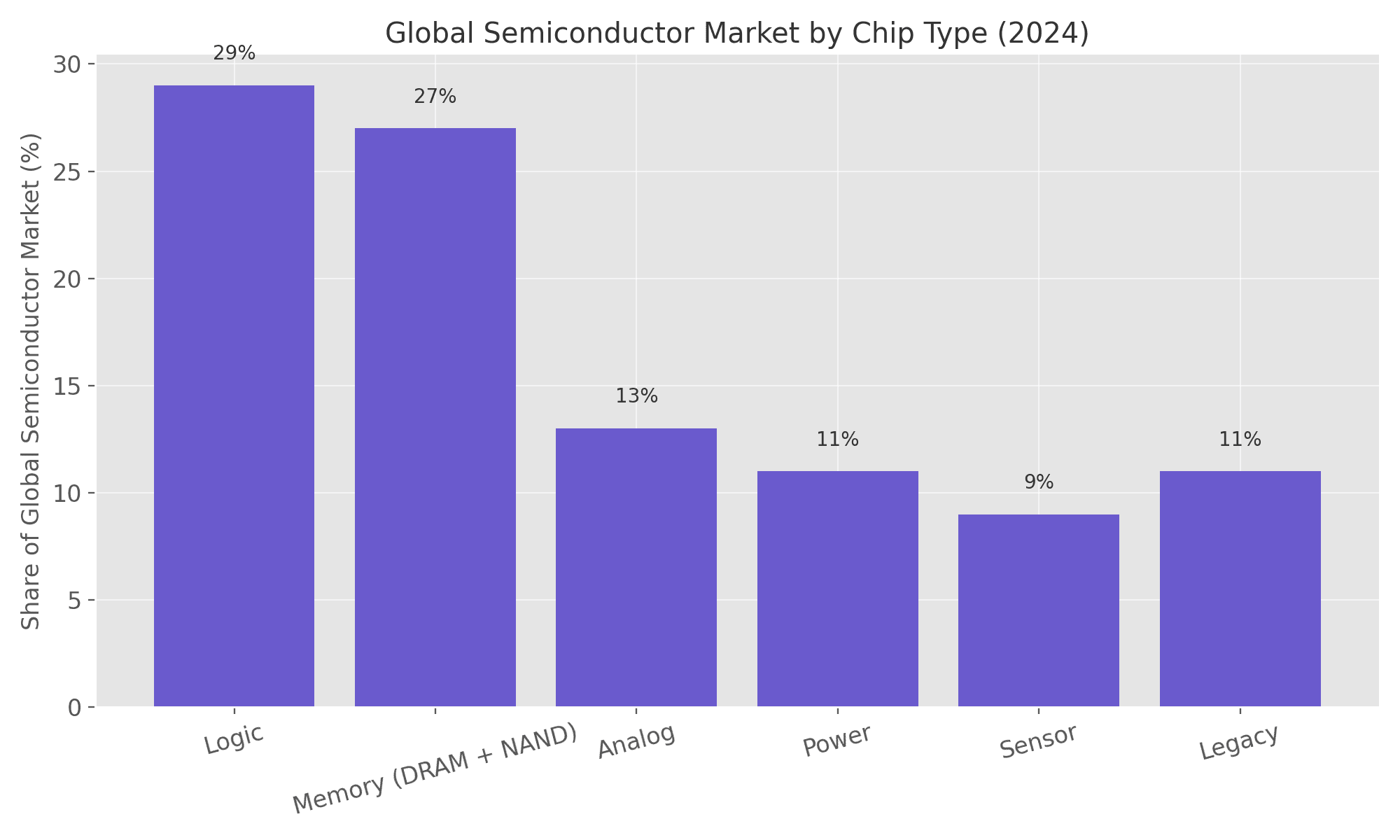

Logic Chips: These are chips that perform computation or control functions – for example, microprocessors, CPUs, GPUs, AI accelerators, DSPs, FPGAs, and microcontrollers. Logic chips execute software instructions and make decisions in electronic systems. Companies like Intel, AMD, NVIDIA, and Qualcomm design high-end logic chips (processors for PCs, servers, smartphones, etc.). These chips are typically manufactured on the most advanced nodes to maximize performance. For instance, Apple’s M1/M2 processors (designed in the U.S.) are fabricated at 5nm in Taiwan to pack tens of billions of transistors on a single chip. Logic chips are crucial for computing power in everything from data centers to fighter jets.

Memory Chips: These chips store data. The main types are DRAM (dynamic random-access memory), which a computer uses for working memory, and NAND flash, used for long-term data storage (like in SSDs, USB drives). There are also other memory types (SRAM, NOR, emerging ones like MRAM/ReRAM, etc.). The memory market is distinct and highly concentrated: South Korea’s Samsung and SK Hynix, and the U.S.’s Micron are the top DRAM makers, while Samsung, Japan’s Kioxia (with U.S. partner WDC), Micron, and SK Hynix dominate NAND flash. Memory chips often require different process technology (not as transistor-dense as logic, but with other complexities like 3D stacking for NAND). South Korea currently leads in memory – e.g., Samsung and SK Hynix together have about 70% of the DRAM market. China has tried to enter this segment (SMIC, Changxin Memory for DRAM, and YMTC for NAND), and by 2022 Chinese firms held ~18% of global DRAM fab capacity (mostly older tech) roc-taiwan.org. Memory is critical for everything that stores information – without DRAM and flash, none of our devices or servers would function. So control over memory technology is also strategically significant (though the geopolitical focus has often been slightly more on logic chips, which are the “brains” performing the operations).

Advanced Node (Leading-Edge) vs. Legacy Node Chips: In chip manufacturing, “node” refers to the technology generation, often described by a transistor gate length (in nanometers, e.g. 14nm, 7nm, 5nm) – smaller is more advanced (though the nomenclature is a bit marketing-driven now). Advanced node chips generally mean the latest, smallest geometries that pack the highest transistor counts (currently 5nm, 3nm, and soon 2nm). These offer the best performance and power efficiency, and they are critical for high-end processors, AI accelerators, and other cutting-edge applications. Only TSMC and Samsung can manufacture at these leading-edge nodes today (Intel is trying to catch up). On the other hand, legacy (mature) node chips refer to those made on older processes: by one common definition in the U.S. CHIPS Act, any chip made on a 28nm or larger process is considered “legacy”csis.org. These legacy chips are larger, less transistor-dense, and typically perform more basic functions – but they are incredibly important. As a CSIS report highlighted, the 2020 chip shortage was overwhelmingly due to inadequate availability of legacy chips, which impacted cars, appliances, and even certain defense systems. Legacy doesn’t mean obsolete – automobiles, industrial machines, medical devices, and some military hardware rely on chips in the 28nm, 45nm, 65nm, etc. range, because those are proven technologies with high reliability. In fact, 80%+ of chips sold globally are manufactured on nodes larger than 28nm, often in older fabs which are fully depreciated and efficient for high-volume, lower-cost production. It’s worth noting that what is “advanced” and what is “legacy” is a moving target – today’s 7nm will be legacy tomorrow. But as of 2025, “advanced” generally means sub-10nm for logic (and the equivalent 1z nm class for DRAM, etc.). Geopolitical angle: The U.S. export controls focus on denying China the advanced nodes, while being less concerned about legacy tech. But ironically, China has become quite capable at legacy-node production (and dominates some of it), which still gives it a foundation to supply many industries. Conversely, the U.S. and Europe realized that ignoring legacy chip manufacturing led to those capabilities moving to Asia (Taiwan, China, Malaysia, etc.), causing bottlenecks. So there is now renewed interest in also securing legacy fabs at home for resilience. The U.S. CHIPS Act even carves out funds for legacy chip production, especially for automotive and defense uses.

Innovation Trends: Pushing the limits of Moore’s Law has become extremely challenging. The latest 3nm fabs cost over $15 billion to build, and each shrink in transistor size requires breakthroughs like EUV lithography (which itself took decades to implement). The complexity of production is astounding – a cutting-edge chip can require over 1,000 process steps and absolute purity in materials. Leading firms now talk about “More than Moore” – i.e., innovations beyond just shrinking transistors. This includes chiplet architectures (dividing a chip into multiple dies and packaging them together), 3D stacking of chips, advanced packaging techniques, and integrating new materials like gallium nitride (GaN) or silicon carbide (SiC) for power electronics. These innovations are also part of the competition. For example, if one country masters 3D integration better, they could leap ahead even without the smallest node. R&D intensity in semiconductors is very high – the industry averages about 15-20% of revenue reinvested into R&D, among the most of any sector. Companies like Intel spend ~$15B annually on R&D, TSMC and Samsung likewise. Governments are injecting research funds too (e.g., the US CHIPS Act directs ~$11B to advanced semiconductor R&D initiatives, and the EU Chips Act similarly sets aside research funding). Key research frontiers include next-gen lithography, new transistor architectures like Gate-All-Around FETs, quantum computing elements, and semiconductor materials.

In summary, not all chips are equal – logic chips vs. memory chips serve different needs, and bleeding-edge chips vs. mature chips both have strategic value. Policymakers must ensure access to advanced nodes (for leadership in AI/supercomputing) andlegacy nodes (for keeping industrial supply chains running). The current tech war often centers on the cutting-edge, but control of “mundane” older chips can be just as consequential in a crunch.

Geopolitical Frictions: Tech Wars, Trade Bans, and the Race to Subsidize

The intersection of geopolitics and semiconductors has led to a flurry of government actions in recent years. The U.S.-China “tech war” over chips has seen export bans and blacklists, while nations worldwide are rolling out subsidies and alliances to bolster their chip sectors. Here we examine the major flashpoints and policy moves shaping this new Cold War over microchips:

The U.S.–China Tech War on Chips

Tensions between the United States and China over technology have increasingly focused on semiconductors. The U.S. goal has been to constrain China’s access to cutting-edge chips and equipment, slowing China’s technological and military rise.

China, for its part, views U.S. actions as a blatant attempt to maintain an unfair monopoly on high-tech and is seeking ways to circumvent or retaliate against these measures.

Export Controls on Advanced Chips: A key escalation came in October 2022, when the U.S. Commerce Department announced sweeping export controls effectively barring Chinese companies from obtaining high-end chips or the tools to make them. These rules prohibit sales to China of GPUs or AI accelerators above certain performance (measured in TOPS), unless a license is granted (which is unlikely for Chinese military-linked end users). It also forbids U.S. persons from supporting advanced fabs in China. Critically, these U.S. rules have extraterritorial reach – they apply to foreign firms if the products contain U.S. technology (which most chips and tools do). Subsequently, the U.S. added specific Chinese chip firms (like SMIC, YMTC, Huawei’s chip design arm HiSilicon) to its Entity List, cutting them off from U.S. tech. Nvidia openly stated it can no longer sell its top AI chips (A100/H100) to China; instead, they created a reduced-performance version (A800) to comply with the limits, illustrating the impact.

Allied Cooperation – ASML and beyond: Knowing that China could try to get equipment from other countries, the U.S. worked to get the Netherlands and Japan on board. By early 2023, the Dutch government agreed to block ASML from selling even slightly older deep-UV lithography machines to China, and Japan imposed similar restrictions on its equipment exporters. This closed off China’s access to virtually all advanced fab tools globally. The chip alliance also extends to intelligence-sharing and coordinating investments among the U.S., Japan, Netherlands, Taiwan, and South Korea – essentially a coalition to ensure China cannot easily source what one country denies from another. These measures have dramatically slowed China’s ability to advance in chip fabrication. For example, without EUV, China cannot manufacture at 7nm or below in high volume; without high-end etching and metrology tools, yields suffer.

Chinese Counters and Tensions: China has denounced these export controls as “technological containment.” It filed a dispute at the WTO (though such processes are slow). More directly, China has taken retaliatory steps: in May 2023, Beijing banned certain Chinese critical infrastructure operators from purchasing Micron’s memory chips, citing security concerns – widely seen as retaliation against the U.S. (Micron is a leading U.S. DRAM/NAND supplier) euronews.com. Then, China’s Commerce Ministry announced in July 2023 export restrictions on gallium and germanium – two minor metals essential in making semiconductor compound materials and some chips – requiring special licenses for any company shipping those abroad csis.org. Since China produces the vast majority of these metals globsec.org, this move threatened to disrupt supply for certain chip makers (for instance, gallium is used in GaN chips which are critical for 5G amplifiers and radar). The message was that China can also inflict pain by leveraging its stranglehold on some raw materials (similar to how it did with rare earth metals in the past). Additionally, there are fears China could restrict exports of other tech-critical materials or even finished electronics if provoked further.

Cyber and IP Battlefronts: The chip war is not only about trade regulations; it’s also played out in industrial espionage and IP. The U.S. has accused Chinese entities of IP theft in semiconductor tech, and both sides are ramping up cyber capabilities to spy on or sabotage each other’s chip-related operations if needed. Taiwan, being a crucial node, has had to crack down on Chinese attempts to poach its engineers or steal secrets from TSMC.

Overall, the tech war over chips is now a central theater in U.S.–China strategic competition, with high stakes. As of 2025, the U.S. retains a strong upper hand: China cannot currently produce the top-end chips needed for state-of-the-art AI or military systems at scale, and its chip firms are feeling the squeeze. But China is investing and innovating to reduce these vulnerabilities in the long run. How this contest unfolds will significantly shape the balance of power in technology.

Subsidies, Alliances, and the New Industrial Policies

At the same time as they wage trade wars, countries are heavily investing at home to onshore production and foster innovation. A new era of semiconductor industrial policy has dawned, with governments committing unprecedented sums to support their chip industries and secure supply chains.

United States – CHIPS and Science Act: We discussed the CHIPS Act’s manufacturing grants ($39B) and R&D programs ($13B) earlier. In addition, the U.S. is offering a 25% investment tax credit for semiconductor manufacturing equipment/facilities (estimated worth another ~$24B). This has led to a boom in fab investment announcements: over $210B in private investment across 20 states as of late 2023, for new or expanded fabs usitc.gov. The U.S. is also establishing the National Semiconductor Technology Center (NSTC) and advanced packaging centers to push next-gen tech. The goal is not just more fabs, but also rebuilding an ecosystem of suppliers and talent. Crucially, companies that take CHIPS Act money are restricted from expanding in China – aligning with the strategy to prevent subsidized firms from simultaneously boosting a potential adversary’s capacity.

Europe – European Chips Act: The EU Chips Act similarly aims to mobilize €43B for the European chip sector to double its global market share lab.imedd.org. Germany, France, Ireland, and others are offering huge incentives to attract fab projects. For example, Germany approved €14B in subsidies for Intel’s planned Magdeburg fab. France is backing a new STMicro GlobalFoundries fab with €5.5B. The EU is also easing state aid rules for chip investments. Alongside fabs, Europe is funding chip design startups, pilot lines, and research (e.g., through the 2030 Digital Compass plan). This is a remarkable turn for Europe, which traditionally relied more on market forces; now it’s unabashedly in the subsidy game to avoid falling behind.

China – Massive State Support: China has arguably been subsidizing chips all along (via state funds, cheap loans, etc.), but it’s upping the ante. The aforementioned $143B package reuters.com is part of a broader strategy including tax breaks (e.g., tax exemption for 5 years for firms making 28nm chips or better), and huge capital for its “Big Fund” second phase (which invested in YMTC, SMIC, etc., though some of that has been mired in corruption probes). Local provinces also shower chip projects with incentives, sometimes leading to inefficiencies or overcapacity in low-end segments. Beijing is also luring back overseas Chinese engineers and pushing universities to expand microelectronics programs to address the talent gap. Despite the U.S. curbs, China is determined to build its own supply chain – from developing indigenous lithography machines (Shanghai Micro Electronics Equipment (SMEE) working on a 28nm-capable tool) to ramping domestic chip fabrication for 28nm and above (SMIC and others are building multiple new fabs for mature nodes, which are not barred and remain lucrative, e.g., for auto chips).

Taiwan and South Korea – Incentives to Stay Ahead: Taiwan, wary of others attracting its crown jewel companies, has introduced its own incentives. In 2023, Taiwan passed new tax credits (up to 25% of R&D expenditures and 5% of capital investment can be credited against taxes) for chip firms that invest domestically. This was informally dubbed Taiwan’s version of a chips act, aimed at keeping TSMC and others pouring money into local fabs rather than just overseas. South Korea, for its part, launched the “K-Chips Act” which improves tax breaks (up to 15% or more) for semiconductor investments, and the government pledged to support the massive private investments (like Samsung’s $230B plan over next 20 years to build new fabs in Korea) with infrastructure and expedited permits. South Korea is also coordinating R&D through its national programs to remain a memory leader and compete in foundry.

Alliances and Cooperative Initiatives: Beyond money, countries are teaming up. The “Chip 4” alliance (US, Japan, South Korea, Taiwan) has been discussed as a forum for coordinating supply chain security. The Quad (US, India, Japan, Australia) has a working group on semiconductors to help diversify manufacturing (India, notably, is vying to become a player by attracting a fab with hefty subsidies; while it has yet to successfully land a major fab, talks with TSMC and others continue, and India is investing in chip design talent and compound semiconductor fabs). The U.S. and EU have a Trade and Technology Council (TTC) where semiconductor cooperation is a key topic – including early warning systems for shortages and aligning on standards/export screening. These alliances are about collective resilience: ensuring if one link in the chain goes down (due to conflict or disaster), others can pick up slack, and ensuring unfriendly powers can’t exploit dependencies.

In essence, there is now a global subsidy race and strategic alignment underway on semiconductors. This is a marked shift from just a few years ago, when chips were considered a mostly private sector domain. Governments have concluded that market forces alone won’t guarantee national security or supply stability in chips – so they are directly intervening with big dollars and policies. This carries some risks: it could lead to oversupply in the long term or inefficient allocation, and it strains trade relationships (every country can’t have 20% of the market – someone’s subsidies will outgun others). But politically, the momentum to “bring the chips home” is strong and likely irreversible in the near future.

Taiwan’s Strategic Vulnerability and “Silicon Shield”

No discussion of chip geopolitics is complete without focusing again on Taiwan’s situation. The island’s leading-edge chip capacity is a unique strategic asset – some call it the “silicon shield” that deters a Chinese invasion, under the logic that China wouldn’t want to destroy fabs it needs, and the U.S. would be compelled to defend Taiwan to protect the world’s chip supply. Indeed, former U.S. officials have openly said TSMC’s fabs make Taiwan critical to global (and U.S.) interests. However, there’s an opposing fear of a “silicon trap”: that reliance on Taiwan tempts China to seize these assets.

The ongoing military tensions – Chinese military drills around Taiwan, concerns of a potential conflict in the 2025–2035 timeframe – cast a shadow over the semiconductor industry. War over Taiwan would be catastrophic for the tech world: A TSMC shutdown, even temporarily, could cost global electronics companies hundreds of billions, and create a deep recession due to tech scarcity. This is why companies are hedging – TSMC is building fabs in Arizona and Japan, so that in a worst-case scenario there are at least some operations outside Taiwan. The global community is in a delicate balancing act: supporting Taiwan’s security (the U.S. frequently reiterates that any forceful change of status quo is unacceptable) while also reducing the potential hostage value of its chip industry by copying its success elsewhere.

From Taiwan’s perspective, its semiconductor dominance gives it “strategic importance that far outweighs our size,” as officials have noted. It’s leveraging that to integrate with the world – e.g., TSMC partnering in the U.S. and Europe – to make sure many stakeholders have an interest in Taiwan’s stability. But it is also aware of the risks; plans are in place to “shut down” or render useless the fabs if they were about to fall into hostile hands, according to some analysts, since the advanced processes cannot be easily continued without the collaboration of the teams in Taiwan (and perhaps equipment vendor support).

In summary, Taiwan’s situation exemplifies the geopolitical entanglement of microchips: a tech asset that boosts its security in some ways, but also attracts geopolitical risk. How the Taiwan question is navigated in coming years is probably the biggest wildcard for the global semiconductor outlook.

Data and Trends: By the Numbers (2025)

Before concluding, let’s summarize some up-to-date data that illuminates the current state of the chip race:

Global Market Size: After a record high of $555.9B in 2021 and a dip in 2023 (to ~$527B), the semiconductor market rebounded strongly. 2024 is estimated at $627 billion in sales futurumgroup.com. Monthly sales in early 2025 are trending upward – e.g., March 2025 saw $55.9B in global semiconductor sales, up ~18.8% year-on-year. Analysts forecast the market could reach $700B by 2025 and around $1 trillion by 2030 usitc.gov, fueled by demand for AI, automotive, and IoT devices.

Market Share by Company Origin: U.S.-headquartered firms hold about 46% of global semiconductor sales (by revenue), thanks to giants like Intel, Qualcomm, Broadcom, AMD, etc. South Korean firms (Samsung, SK Hynix) are next with roughly ~19–20% (especially due to memory market). The remaining share is split among companies from Japan (~10%), Europe (~10%), Taiwan (~7–8%), and China (~6–9%). Notably, Chinese semiconductor companies still only account for a single-digit share of global sales (despite China consuming over 30% of chips), reflecting China’s dependence on foreign tech – although China hopes to raise its share to 25% by 2030.

Manufacturing Capacity by Location: As shown earlier, 75% of global chip manufacturing capacity is in East Asia (Taiwan, South Korea, Japan, China) usitc.govusitc.gov. Taiwan and South Korea alone contribute nearly half of worldwide capacity (especially at advanced nodes). The U.S. has about 11-12% of fab capacity, and Europe around 9%, as of 2021. China’s share is ~16% and growing. The concentration in Asia (Taiwan/Korea) is even more extreme for leading-edge logic: ~92% of <10nm capacity in Taiwan, ~8% in South Korea (Samsung), effectively 0% in U.S./Europe/China at present. For memory, South Korea has ~44% of global wafer capacity (Samsung, SK) usitc.gov. These imbalances are what many of the new policies seek to address by building more fabs in the U.S. and Europe.

R&D and Capital Intensity: The semiconductor industry spent over $70 billion on R&D in 2022, and that number keeps risingsemiconductors.org. U.S. semiconductor firms alone invested $47B in R&D in 2021ncses.nsf.gov. It’s an R&D-intensive industry (averaging ~18–20% of revenue), second only to perhaps pharmaceuticals. Capital expenditures (CapEx) are also huge: TSMC, for example, spent a record $36B on CapEx in 2022; Samsung and Intel similarly spend tens of billions annually to build new fabs. These enormous investments create high barriers to entry – which is why nations are pooling public money to help. Government R&D: The EU is allocating €5B to chip R&D centerslab.imedd.org; the U.S. is setting up the NSTC and advanced packaging institute with ~$11B; Japan has put money into joint research with industry (like with IBM for 2nm tech). The objective is to push the next breakthroughs (like EUV 2.0, quantum chips, etc.) and not cede leadership.

Talent and Workforce: The chip industry faces a talent crunch. There is high demand for semiconductor engineers, but the field is specialized. The U.S. projects a need for tens of thousands of additional skilled workers for the new fabs; programs to train and attract talent (including international engineers) are ramping up. China has expanded semiconductor engineering programs massively, but still lacks enough experienced veterans in cutting-edge design and manufacturing – leading it to headhunt from TSMC, Samsung, etc. Taiwan and Korea continue to churn out skilled engineers but also face poaching pressures. Countries recognize that spending on fabs alone isn’t enough – human capital development is equally critical.

These numbers and trends paint the current picture: robust growth in demand, dominant positions by a few players, and a heavy focus on advanced tech and investments. They set the stage for considering how the next phase of the chip race might unfold.

The Road Ahead: The Chip Race in the Next 5–10 Years

Looking forward, the geopolitics of microchips will likely intensify further. The “Chip Race” – the competition to achieve or maintain dominance in semiconductor technology – will be a defining feature of international relations and economic strategy in the coming decade. Here are some key forward-looking insights and scenarios for the next 5–10 years:

Bifurcation vs. Interdependence: One big question is whether the global chip supply chain will splinter into two blocs – a U.S.-led sphere and a China-led sphere – or remain interdependent. If U.S. export controls persist and China keeps pushing for self-reliance, we could see a bifurcated tech ecosystem by 2030: with one set of chip companies (TSMC, Samsung, Intel, etc.) serving the U.S/allies with ultra-advanced chips, and another set (SMIC and Chinese firms) producing good-enough chips for China and aligned nations. China might develop its own versions of technologies (e.g., Chinese lithography machines, China-only EDA tools and chip IP). This decoupling would reduce the vulnerability of each side to the other, but at the cost of huge efficiency losses and duplication. It could also drive up costs globally (losing economies of scale) and slow innovation (less cross-pollination of ideas). On the other hand, full interdependence as before is unlikely to return, given trust issues. The likely outcome is something in between: a partial decoupling where China attains self-sufficiency in mature nodes and certain chips (like power electronics, older logic, memory), but remains behind or shut out of the extreme leading edge; meanwhile the U.S. and allies diversify away from China for critical chip needs but still rely on each other.

Technology Trajectories: By 2030, industry leaders plan to move from today’s 3nm node to 2nm and even 1.4nm (in nomenclature) for logic. IBM has prototyped a 2nm chip, and TSMC, Samsung, Intel all have roadmaps for 2nm around 2025–2026. These will involve new transistor structures (gate-all-around nanosheet transistors), likely requiring ASML’s next-gen High-NA EUV machines (which are even more precise). If current trends hold, TSMC and Samsung will implement these first, possibly joined by Intel if it executes well on its comeback plan. China is very unlikely to reach those nodes by 2030 without access to Western tech. So the tech gap might actually widen if export controls persist. One wild card: quantum computing – if practical quantum machines emerge (which rely on very different “qubits” rather than classical transistors), could that leapfrog current chips? Probably not replacing semiconductors in 5-10 years, but it could augment certain specialized computing tasks.

Alternate Approaches: We will also see more emphasis on chip packaging and integration as Moores Law slows. Advanced packaging (like TSMC’s SoIC, Intel’s Foveros) can stitch multiple chiplets into one, achieving performance gains. The U.S. is investing in leading packaging capabilities to possibly offset not having leading-edge fabs for a while. If the U.S. or Europe can become hubs for advanced packaging, they might circumvent some dependence (e.g., get slightly less advanced chips from multiple sources but package them in ways that yield cutting-edge performance). China, interestingly, is quite active in advanced packaging too (as it can do that without EUV). So packaging might become a more level playing field competitive space.

Regional Shifts: By 2030, we can expect the geographical mix of chip production to even out slightly. The U.S. might rise from 12% to maybe ~15%+ of global capacity if new fabs ramp up. Europe might go from ~9% to, optimistically, mid-teens% if Intel and others succeed. China’s share could approach the mid-to-high teens (perhaps ~20% if their expansions succeed, mostly in legacy nodes) worldpopulationreview.com. Taiwan and South Korea may reduce a bit in percentage (not necessarily in absolute output) if others grow, but they will still be central. This diversification is good for resilience – more distributed capacity. But it will take years for those new fabs to come online and yield; some projects may face delays or cost overruns. The next 5 years are just the beginning of that shift.

Supply Chain Security and Stockpiling: We may see more stockpiling of critical chips by governments. Already, some countries have strategic reserves of oil; in the future, they might maintain strategic reserves of semiconductors (especially for defense and essential industries). China reportedly built up inventories of certain chips ahead of U.S. sanctions. The U.S. DoD ensures it has a two-year supply of certain radiation-hardened chips. This trend could continue, although chips have shelf lives and obsolescence, making it tricky.

Collaboration in Research: Amidst competition, there could be areas of collaboration – for example, standard-setting for chip security (ensuring chips are free from hardware trojans, etc.), or environmental aspects (semiconductor manufacturing is resource-intensive; global cooperation might arise in making the industry greener, reducing its carbon and water footprint). Chip production uses toxic chemicals and lots of energy; as fabs spread, there will be more focus on sustainable practices, which could be a shared goal across countries.

Potential Conflict Scenarios: The worst-case scenario for the chip world would be a military conflict over Taiwan. While not inevitable, planners must consider it. Such an event would likely cause a severe disruption in chip supply for months or years. It might accelerate the formation of an entirely separate Chinese supply chain (if China takes control of facilities or at least removes its reliance on others out of necessity). It would also dramatically boost U.S. and allied domestic production efforts in emergency mode. Basically, the shock would rewire the industry. Everyone hopes to avoid this scenario by maintaining deterrence and diplomatic stability in East Asia. In the meantime, companies like TSMC having some capacity in Arizona and Japan by 2025–2027 is a kind of insurance.

Innovation Wildcards: There is always the chance of a technological wild card – e.g., a breakthrough in AI chip design that allows much simpler production, or new architectures that use more mature nodes but clever design to achieve performance (for instance, RISC-V open architecture could allow many players to innovate in custom chips without x86/ARM). China is investing in optical computing and other non-traditional approaches – if they found a way to mitigate its dependence on nanometer-scale lithography by using a different computing paradigm, that could alter the race. However, most experts feel nothing will replace mainstream semiconductor scaling for the next decade; thus the race remains on who can make the smallest, fastest, most efficient chips.

In conclusion, the next 5–10 years in the geopolitics of microchips will be characterized by accelerated competition and heavy investment. Semiconductors have truly become a geostrategic commodity, and nations will treat them as such – guarding supply chains, fortifying domestic industries, and jostling for technological leadership. The “new Cold War” framing might actually intensify, as each side tries to avoid dependence on the other for chips while seeking any advantage. Yet, unlike the Cold War of the 20th century, this is not an ideological battle – it’s a race grounded in industrial capacity and innovation.

Who will “win” the chip race? It may not be a zero-sum game; multiple regions can thrive if they find niches and cooperate on some levels. The U.S. and its allies currently hold the high ground in chip technology – and are poised to maintain it if they execute on current plans – but China’s sheer focus and scale means it cannot be counted out. What is certain is that microchips will remain at the heart of global geopolitics for the foreseeable future, and decisions made in silicon labs and fabs will echo in the halls of power worldwide. As the world becomes ever more digital, the nation(s) that lead in producing the “brains” of our machines will significantly shape the economic and security order of the 21st century.

Sources: The analysis is supported by data and insights from industry associations (Semiconductor Industry Association), government reports (US ITC, CSIS), news agencies (Reuters, Politico, The Economist), and expert commentary, as cited throughout llab.imedd.org , worldpopulationreview.com knometa.com comcsis.org. These sources provide context on semiconductor market shares, government policies like the CHIPS Acts, and the strategic importance of various chip types and geographies.

Stay tuned to The Horizons Times for continuing coverage on the evolving semiconductor landscape and the strategic implications shaping our digital future.

Oleksandr Vovchok

Author in the field of digital and science.

Prev Article

India hits militant sites in Pakistan and Kashmir amid cross-border tensions

Next Article

India launches Operation Sindoor, targets militant sites in Pakistan

Leave a Comment